No Score Loan With Manual Underwriting

No credit check loans: clear your doubts over such a loan 4 ways student loans can help your credit score Underwriting scoring loan profound pandemic undergo

What credit score is needed for an unsecured personal loan? Leia aqui

Decentralized underwriting Obtain a no score loan through manual underwriting: overcome debt and Manual underwriting magic: getting a mortgage with no credit score

What credit score is needed for an unsecured personal loan? leia aqui

Get your mortgage loan approved – know the 4 cs of underwritingHow to get a personal loan with low credit score and lack of documents No credit scoreManual underwriting mortgage loan.

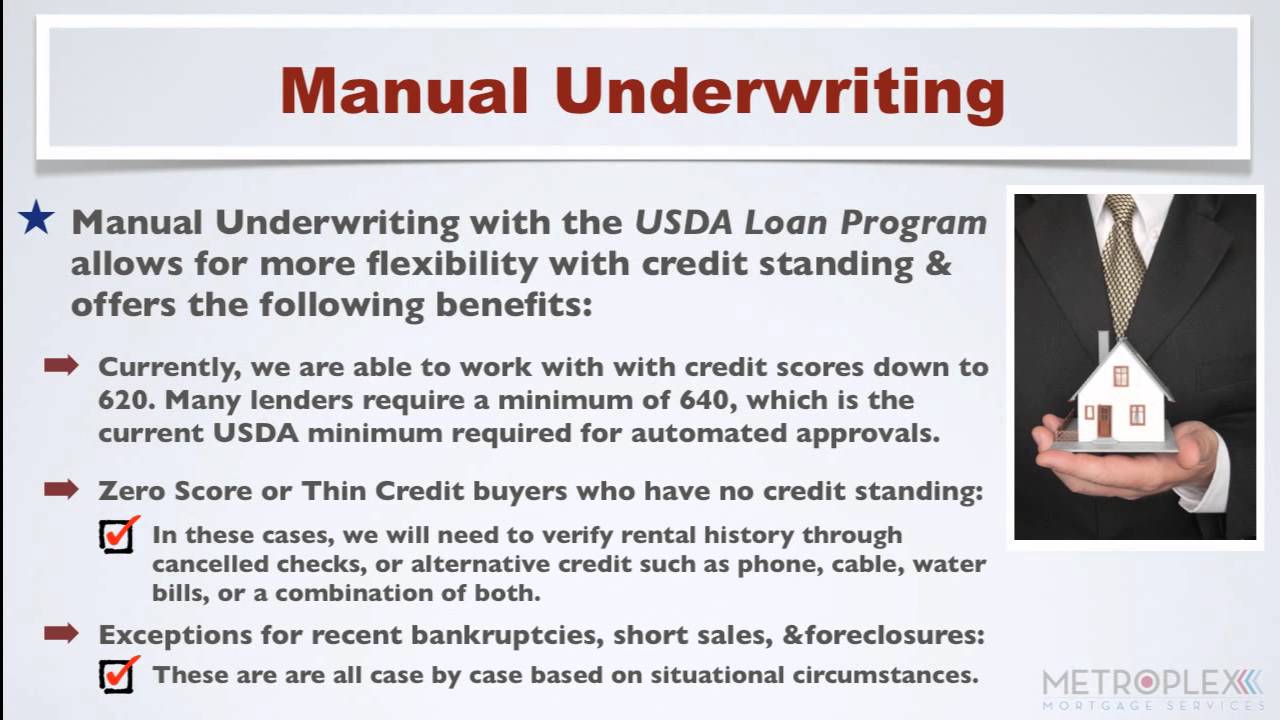

How do loans work?What is manual underwriting and can it help you qualify for a usda loan The mortgage underwriting process explainedVa manual underwriting guidelines for va loans.

Explaining manual underwriting on va loans

No credit scoreFha manual underwriting & va loan manual underwriting guidelines No credit score manual underwritingGuidelines underwriting manual credit loans fha va 27th published updated january.

Du job aids: viewing and printing the du underwriting findings andUnderwriting manual Underwriting & psas – wrfg 89.3 fm atlantaHow to qualify for a conventional loan with no credit score.

Manual underwriting credit guidelines on va and fha loans

Underwriting manual fha loanUnderwriting loan Underwriting automated system psasManual underwriting magic: getting a mortgage with no credit score.

Online demonstrationNo score loan through manual underwriting Is manual underwriting more expensiveManual underwriting no credit.

Can you buy a house with no credit score?

Underwriting loanSolved the loan is automatically rejected if the applicant's Underwriting vaThe smart reasons why high-score borrowers take out personal loans.

Loan underwriting demoLoan underwriting: 4 ways credit scoring may undergo profound changes Conventional loan manual underwriting: your application's second chanceLoans loan payday.

29+ mortgage underwriting salary

.

.

{kind=link}